A Smarter Way to Stop Leaks: In Your Home & Your Wallet

Protect Your Home from Water Damage: The Importance of Shut-Off Valves and Smart Water Devices

Water damage is one of the most frequent and expensive insurance claims homeowners face. A single burst pipe or undetected leak can cause thousands of dollars in damage. Fortunately, one of the most effective ways to prevent major water loss is simple: knowing where your main shut-off valve is—and making sure it works. As most people forget to turn off the water when they leave for an extended time to prevent damage, a new concept has hit the markets with great success: smart water devices.

From Old School to High Tech

While manual valves are essential, newer smart water monitoring and shut-off systems offer even more protection. These devices monitor water flow in real time and can automatically shut off water if a leak or unusual usage pattern is detected—whether you're home or away. It has proven a successful enough alternative that several insurance carriers have started to give discounts or full water damage coverage rather than limited water damage coverage to those who buy the system.

Popular systems include (but are not endorsed by this agency, just some ideas of brands to get you started on your research):

- Flo by Moen

- Phyn Plus

- LeakSmart

- Guardian Leak Prevention System

Some models integrate with home automation platforms and can send alerts directly to your smartphone. There are various levels to research when considering this:

- Level 1: A sensor-based water leak detection system that notifies customers via mobile device/internet connection when a leak is detected. (lowest discount)

- Level 2: A sensor-based water leak detection system that automatically shuts off the water supply to the home when a leak is detected (mid-range discount)

- Level 3: A water leak detection system that assesses water flow through the plumbing and automatically shuts off main water supply to the home when a leak is detected.

How Level 3 Works:

- Installs on the main water supply line and proactively monitors the home for leaks as small as a drop per minute

- A water leak detection system that assesses the flow of water through the plumbing

- If an issue is detected with the home's plumbing, receive real-time alerts from the mobile device

- 24/7 monitoring with remote shut-off

- The device will automatically turn off the water supply to the home should a major leak be detected

Insurance Benefits AND Peace of Mind

Smart water protection systems not only help prevent catastrophic damage—they can also lead to insurance premium discounts. Many insurers recognize these devices as proactive risk mitigation tools and may offer policy credits for installing them. Some, as previously mentioned, will even give full non-weather related water coverage where they would usually limit at $10k. Those who have implemented this discount & coverage practice have seen drastic reduction in the water-related claim activity, meaning homeowners are not experiencing claims due to water leaks as much as prior to advocating for these systems. Because of this success, most carriers have indicated they will be implementing the shut-off system discount/coverage concept in the near future.

Tips for Homeowners:

- Locate and label your main manual shut-off valve

- Test it at least twice a year to ensure it's working

- Consider installing a smart leak detection and shut-off system—especially in vacation homes or properties that are unoccupied for extended periods

- Let us know if you have any questions

Bottom Line

Water shut-off valves and smart leak detection systems are simple yet powerful tools for protecting your home. Investing a little time—and possibly some smart technology—can save you from major headaches, repair costs, and insurance claims down the road, not to mention saving you money on premiums.

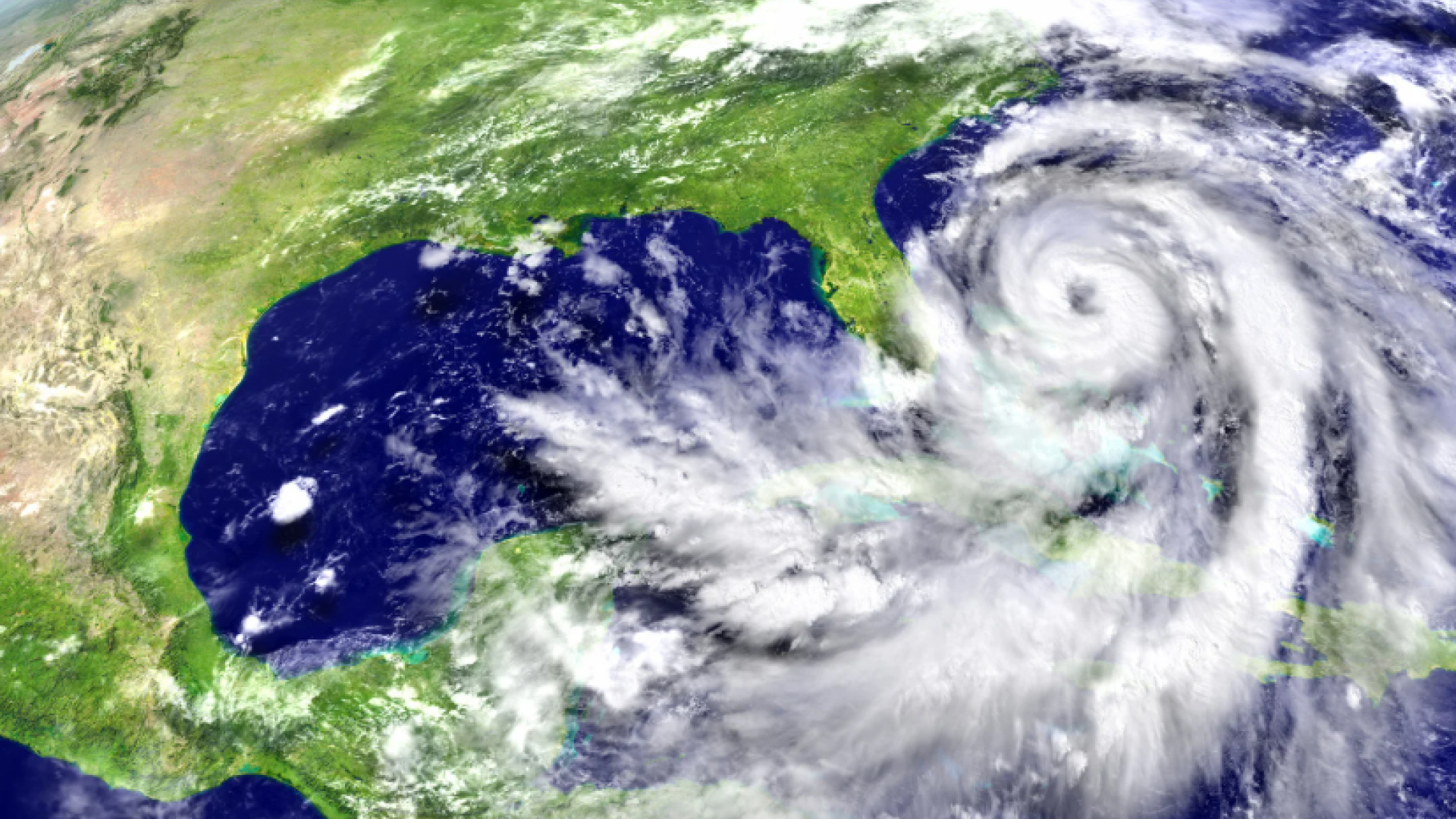

Storm Season 2025: Be Prepared and Protected

Stay ahead of the storm – check back monthly for protection tips and insurance guidance throughout the 2025 storm season.

- At least twice a year, it is recommended that you open all cabinets, drawers, closets, etc. and take pictures or videos on your phone or ipad throughout your home. Documenting the interior and exterior will help -+ This will help you with an inventory list should you sustain damage and provide proof if asked that you owned specific items.

- For NFIP (FEMA) flood policies, they will reimburse up to $1,000 for loss avoidance measures taken when flooding is imminent. This includes sandbags, pumps and lumber.

- Avoid using sandbags if possible as they can become contaminated and toxic if flooding does occur. Opt for the sandless version instead.

- Check rain gutters to make sure they are clear of debris which can cause water damage issues in a storm.

- Review your chosen coverage limits on all policies. While auto policies typically carry a smaller deductible amount per occurrence, homeowners policies carry high deductibles for storms. There is a difference between “hurricane deductible”, “Named Storm” deductible and “Wind/Hail deductible”. All will be a percentage of the dwelling amount (2%, 5%, 10%) but they apply to different situations. Those deductibles are typically much higher. Hurricane deductibles run per calendar year, not policy period and can not be changed until renewal for any property policy – commercial or residential.

- For up-to-date information and how to file a claim in the event of a storm, click the “announcements” link at the top of the home page.

In the Know: Because Someone Has to Explain This Stuff!

Last month’s greatest hits: frequently asked, always answered.

Q: Why is the carrier coming out to do an inspection of my house?

A: Skip over to the (awesome) section about the history of the concept of insurance titled, "Insurance: Lloyd’s of London Gets the Street Cred, But It Was the Chinese Merchants Who Started It All". After reading that, come back here to finish reading.

Inspections are a standard part of the underwriting process. This is when insurance carriers assess the property to confirm it’s in good condition, hasn’t sustained undisclosed damage, and doesn’t pose avoidable risks—like yard clutter that could turn into airborne debris during a storm.

It’s important to remember: insurance isn’t a maintenance plan. It’s designed to provide financial protection when the unexpected happens—not when a preventable issue becomes a costly one. Inspections help ensure the property is being responsibly maintained and doesn’t represent a “bad risk” or a likely loss.

For example, trimming back overhanging trees can help prevent roof damage during a storm. Clearing shrubs from windows not only minimizes storm damage risk, but also reduces visibility for potential intruders—avoiding what insurers call an “attractive nuisance.”

Ultimately, inspections serve as a checks-and-balances system. They help verify that homeowners are doing their part to reduce avoidable claims, and that properties are insured at values that truly reflect their condition and risk.

Q: Why do I have to show proof of repairs after a claim?

A: Many of the rules, guidelines, and documentation requirements in insurance exist because of past claims and lawsuits—and one of the biggest turning points was Hurricane Andrew in 1992.

After the storm devastated South Florida, insurers issued large claim checks directly to homeowners. But instead of making repairs, many homeowners pocketed the money, abandoned the property, or spent it elsewhere, leaving homes damaged and mortgage companies—and insurers—exposed.

Unrepaired damage often leads to worse problems (like water damage turning into toxic mold), and when that happens, insurance companies are forced to either pay for it or deny the claim and defend that decision in court—which costs money. Lots of it – and it has to come from somewhere!

That’s why today, insurers ask for proof of repairs and perform inspections: they want to avoid taking on “bad risks” that are likely to lead to claims. It’s not just about one property—it’s about protecting the whole risk pool.

Remember, premiums aren’t calculated on individual merits alone. They’re based on the law of large numbers: how many premium dollars need to be collected to cover not just claims, but also legal costs. So, when preventable losses increase, everyone’s rates go up.

Think of it this way: would you knowingly buy a car with major issues, driving it off the lot excited to spend thousands fixing it? Neither would insurers—hence the checks & balances, the guidelines, and yes, the paperwork.

Q: Why did my rates go up, I haven’t had any tickets, accidents, claims and I pay my bills on time?

A: Most of what you’re hearing about proof of repairs ties back to a bigger picture: insurance is built on the law of large numbers. That means insurers have to take in enough premium dollars to cover the claims being paid out—and when claims increase, so does the cost of doing business.

One major factor? Reinsurance—that’s insurance for insurance companies. As claim volume and litigation rise, reinsurance becomes more expensive, and that cost is passed directly to consumers. Reinsurance becomes more expensive when claims become more expensive. Inflation post storms, fraud, litigation costs, etc. all of it translates into either a claim payout or a claim denial that has to be defended, both of which costs money!

And yes, we feel it too. We don’t receive any special discounts for working in the industry. We’re right there with you—shocked at our own renewal rates and just as frustrated by the rising costs.

In Florida especially, a mix of weather events (hello, hurricanes), widespread litigation, and fraud have made premiums unpredictable. It’s not fun, and it’s definitely not fair, but it is the reality of our market right now.

Our best advice? Remember that nothing is truly “free” in life and change starts with people speaking up. So reach out to your State Representatives to voice your concerns and do diligent research anytime insurance related topics are on a ballot.

Let's Clear That Up

Because your cousin's Thanksgiving insurance advice came with confidence, not credentials.

Myth #1: Homeowners Insurance covers flood damage.

Homeowners insurance never covers flood damage. There are some policies out there that have a flood endorsement that will cover up to the dwelling amount of the homeowners policy but homeowners, on it’s own merits, does not EVER cover flood claims.

Myth #2: You don’t need flood insurance outside of high-risk zones.

40% of all flood claims occur in low to moderate risk areas. Keep in mind that flooding can occur anytime, not just during a hurricane.

Myth #3: “Full Coverage” on a Florida auto insurance policy means comprehensive and collision coverage.

“Full Coverage” is one of those magical phrases that make insurance agents pause, take a deep breath, and briefly consider a career in goat farming. “Full Coverage” does not merely mean a policy with comprehensive & collision coverage.

It means:

- Personal Injury Protection

- Medical Payments

- Uninsured Motorist

- Bodily Injury

- Property Damage

- Comprehensive

- Collision

- Rental Reimbursement

- Roadside Assistance

Next time you're chatting with us about your auto policy, confidently tell us what coverage you want quoted. We’ll throw you an imaginary parade (with confetti made of policy declarations pages).

Myth #4: It’s cool for me to change my business model, name and/or owners at any time without notifying insurance.

Nothing could be further from the truth! Commercial insurance doesn’t cover “whatever you’re up to now.” It’s built around a specific legal entity, specific owners, and the specific work you told us you were doing when the policy started.

Change any of that—new owners, a shiny new Corp or LLC, or a totally different line of work—and your policy might not respond when you need it most. Claims can (and often will) be denied, and in some cases, owners could even be on the hook personally.

So if something’s changing in your business—call us. We’d much rather say, “Nope, you’re good!” than, “Oh no… that’s not covered, and you’re going to want clear your calendar and grab a snack for this conversation.”

Insurance: Lloyd's of London Gets the Street Cred, but it was the Chinese Merchants Who Started it All

It’s no secret that insurance isn’t exactly a crowd favorite most days. It’s confusing, tedious and usually only comes up when something goes wrong or when you get the bill. But here’s the thing: insurance actually started as a pretty smart idea, way before it became the headache we all know.

About 2,000 years ago, Chinese marine merchants faced a simple problem: their ships sank sometimes. Instead of losing everything from ship to cargo when one went under, they spread their cargo across multiple vessels. If one ship went down, it was just a bad day, not a catastrophic one as they didn’t lose the whole load. This early risk-sharing tactic is basically the foundation of insurance—simple, practical, and surprisingly effective.

Jump ahead to 17th-century London, where a small coffee house run by Edward Lloyd became the unofficial headquarters for ship owners, traders, and anyone looking to bet on whether a ship would make it back in one piece (true story!). Over cups of coffee (and likely stronger stuff), these early underwriters would agree to take on a portion of a ship’s risk—for a fee, of course. And so the ancient idea of risk pooling was turned into a business.

But here’s where things evolved: Lloyd’s of London didn’t just offer coffee and gossip—it created structure. It formalized risk-sharing into something reliable and repeatable. Policies were written, risks were quantified, losses were paid out (well, most of the time), and the whole process started to look like a real industry.

Underwriters would literally write their names under the amount of risk they were willing to take on—hence the term "underwriter." The system became a marketplace: a central hub where risks could be assessed, divided up, priced, and managed. It was like turning the casual, clever tactics of Chinese sea traders into a full-fledged financial machine.

And that’s how modern insurance was born. Not from a government mandate or a corporate boardroom, but from practical people who wanted to protect their ships—and their wallets.

Still, the idea behind it is solid: share the risk so nobody gets wiped out. Not glamorous, but effective. And honestly, when something goes really wrong, having that confusing, unglamorous safety net in place? It’s a lifesaver. Literally.

So why do we dislike insurance? Because somewhere along the way to becoming an industry, that straightforward idea got tangled up in legalese, fine print and lawsuits. What started as a simple safety net now often feels like a complex maze of clauses and conditions.

Next time you’re frustrated with your policy, remember—it’s just an old-school plan with a modern twist: share the risk so nobody gets wiped out. Not glamorous, but it works. And hey, it’s one of the few things you pay for and hope you never actually have to use—kind of like a gym membership, but with fewer treadmills.

Oliver Off-Duty: The Doxie Diaries

A newsletter within a newsletter, about anything other than insurance, because Oliver refuses to be left out.

It happened just after normal lunchtime. The office was quiet — that lull between the last sip of LaCroix and the first Slack message about “jumping on a quick call.” I was stationed on my “desk” (bed), pretending to nap but fully alert. Always alert.

That’s when I heard it.

The sound.

The crinkle.

Not the loud, frantic crinkle of a vending machine snack — no, this was the stealthy, slow-motion kind. A ziplock bag. Homemade. Possibly illicit.

I moved fast — not bark-fast, but confident and direct, the way a mini dachshund moves when he senses something warm and edible.

There she was trying to act casual, like she wasn’t holding what I knew to be food. She said, “Oliver, this isn’t for puppy dogs.”

And yet... she was holding it so low. Practically an invitation.

I sat. Tilted my head. Did the blink — the one that says I am small, I am polite, and I have not eaten since 1997. Floppy, inquisitive ears deployed. She sighed. Checkmate.

“Fine. One piece.”

She dropped it.

It hit the floor like a gift from the snack gods.

Still warm.

Cheddar. Flaky.

Buttery like a coworker compliment before a deadline.

Ladies and gentlemen: cheddar-chive biscuits!

Yes, it’s as good as it sounds. And yes, she gave me another.

She’s only human.

As part of my ongoing commitment to office transparency—and snack equity—I present the recipe in full:

Cheddar-Chive Drop Biscuits

As approved by Oliver but barely shared with him.

Ingredients:

- 2 cups all-purpose flour

- 1 tbsp baking powder

- ½ tsp baking soda

- 1 tsp salt

- ½ cup (1 stick) cold unsalted butter, cubed

- 1 cup sharp cheddar cheese, shredded

- 2 tbsp fresh chives, chopped

- ¾ cup buttermilk (or milk + 1 tsp vinegar as substitute)

Instructions:

- Preheat oven to 425°F (220°C). Line a baking sheet with parchment paper.

- In a large bowl, whisk together flour, baking powder, baking soda, and salt.

- Cut in the butter with a pastry cutter or your hands until the mix resembles coarse crumbs.

- Stir in cheddar and chives.

- Add buttermilk and mix just until combined (don’t overwork).

- Drop heaping spoonfuls onto the baking sheet — rustic is the goal here.

- Bake 12–15 minutes, until golden and crisp on the edges.

- Let cool slightly... then try to keep your office dachshund from claiming one.